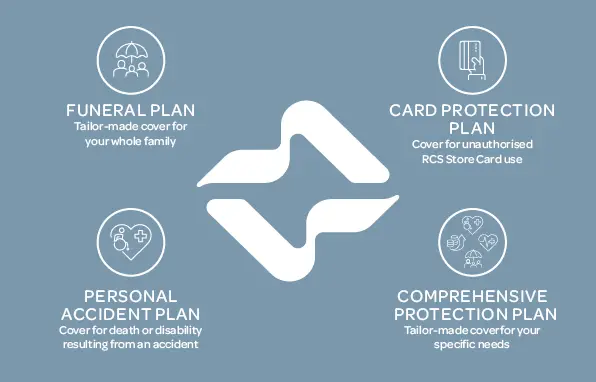

Personal Accident Plan: Takes care of your loved ones if you pass away or become disabled as a result of an accident.

Funeral Plan: Flexible so you can cover yourself, your spouse, up to 5 dependent children and up to 6 extended family members.

Card Protection Plan: You don’t have to worry about unauthorized use on your RCS Store Card if you have taken out our Card Protection Plan. Cover for just R 15 per month.

Comprehensive Protection Plan: Gives you freedom of choice. Death cover and a choice between Severe Illness cover, Permanent Disability cover or an Income Booster with a daily monetary benefit for when you are in hospital.

RCS Insurance is underwritten by Guardrisk Life Limited, an authorized financial services provider (FSP76) and a licensed life insurer, and Guardrisk Insurance Company Limited, an authorized financial services provider (FSP75) and a licensed non-life insurer.